Free Loan Calculator for EMI & Interest Rates

Amortized payments, deferred lump-sum payoff, and zero-coupon present value with compounding and payment frequency options.

Amortized loan: fixed amount paid periodically

Mortgages, auto loans, and personal installment loans usually work this way: the same payment each period until the balance is zero.

Deferred payment loan: lump sum due at maturity

Principal plus all interest is repaid in one payment at the end of the term (no periodic principal payments).

Bond: predetermined amount due at maturity

Zero-coupon style: you know the face amount to be paid at maturity and want the present value (amount received when the loan starts) at a given yield and compounding.

Results are educational estimates. Lenders may use different conventions, fees, or day-count rules; confirm figures on your contract.

Taking a loan is a big financial decision. Before you sign any papers, you need to know exactly how much you will pay every month. That is where a free loan calculator makes all the difference.

For property-specific schedules, also try the Mortgage Calculator; for car price minus down payment, use the Auto Loan Calculator alongside this page.

On this page

What Is a Loan Calculator?

A loan calculator is a simple online tool. You enter three numbers: the loan amount, the interest rate, and the loan tenure. The calculator then instantly tells you your monthly payment.

It uses a standard mathematical formula to give you accurate results. No guesswork. No manual math. Just reliable numbers you can trust.

Main Components Used in Calculations

- Loan Amount (Principal): This is how much money you borrow. In Pakistan, personal loans go up to PKR 4 million, while car loans can reach PKR 3 million. The Auto Loan Calculator is tailored when you already know vehicle price and down payment.

- Interest Rate: This is the percentage the bank charges you for borrowing money. In Pakistan, rates typically range from 9% to 16% per year depending on the loan type.

- Loan Tenure: This is the repayment period, usually measured in months or years. Tenures range from 1 year for short personal loans to 20 years for home loans.

- Monthly EMI: This is the fixed amount you pay every month until the loan is fully paid off.

Together, these four components give you a complete picture of your loan. You can experiment with different values to find the most affordable option for your situation. When you are ready to compare a flat or plot offer line by line, open the Mortgage Calculator as a second tab.

How EMI Is Calculated

EMI stands for Equated Monthly Installment. It is the fixed monthly payment you make to repay your loan.

The formula used is:

EMI = [P x R x (1+R)^N] / [(1+R)^N - 1]

Where:

- P = Principal (the loan amount you borrow)

- R = Monthly interest rate (annual rate divided by 12)

- N = Total number of monthly payments (tenure in months)

Here is a real example to make it clear:

Suppose you borrow PKR 1,000,000 at 15% annual interest for 5 years (60 months).

Monthly interest rate = 15% / 12 = 1.25%

EMI = approximately PKR 23,800 per month

Total amount paid = PKR 1,428,000

Total interest paid = PKR 428,000

Notice that you pay PKR 428,000 extra just in interest. That is why planning your EMI before taking the loan is so important. If you want to contrast that cost with how the same rate would grow savings, glance at a Compound Interest Calculator once you have your loan numbers.

How Each EMI Is Split

Each monthly payment has two parts:

- Interest Portion: In the early months, most of your EMI goes toward paying interest. For example, in month one of the above loan, about PKR 12,500 of your PKR 23,800 is pure interest.

- Principal Portion: As months pass, you pay less interest and more principal. By the final months, nearly your entire EMI goes toward clearing the loan balance.

This structure is called loan amortization. The reducing-balance method used in most Pakistani banks is actually better for borrowers. It charges interest only on the remaining balance, not the full original amount. This saves you more money compared to the flat-rate method. A Simple Interest Calculator shows the opposite idea—interest on the full principal—which is why it is not how most installment loans work.

Features of an Online Loan Calculator

Modern loan calculators offer much more than just a basic EMI figure. Here is what a good online calculator gives you. For housing-only scenarios you can still cross-check with a Mortgage Calculator, and for dealer quotes keep an Auto Loan Calculator handy so price, down payment, and rate stay aligned.

1. Instant EMI Calculation

• Real-time results appear as soon as you type in your numbers

• No waiting, no page refresh, no sign-up required

• Beginner-friendly interface that anyone can use

2. Interest Rate Comparison

Different banks offer very different rates. For instance:

• HBL offers car loans at 12.5% to 15.5% per year

• Meezan Bank offers Islamic car finance at 12% to 15%

• Standard Chartered offers car loans at 9% to 11%

A calculator lets you plug in each bank's rate and instantly see which deal costs less. That comparison could save you tens of thousands of rupees.

3. Flexible Tenure Options

Changing the loan tenure has a huge impact on your monthly payment. For example:

• A 2-year car loan might cost PKR 25,000 per month

• The same loan over 5 years drops to about PKR 15,000 per month

However, longer tenures mean more total interest paid. The calculator shows both sides so you can decide what works best for your budget.

Types of Loans You Can Calculate

A good loan calculator works for all common loan types in Pakistan. Here is a quick overview. Whenever a lender only quotes “per month”, a Payment Calculator can isolate the installment line before you worry about fees or insurance add-ons.

Personal Loan Calculator

• Covers personal expenses like weddings, medical bills, or home improvement

• Pakistani banks offer personal loans from PKR 30,000 to PKR 4 million

• Rates are typically KIBOR + 14-16%, which makes them the most expensive loan type

• Tenures range from 1 to 4 years

Car Loan Calculator

• Helps you plan vehicle financing before visiting a dealership

• Interest rates range from 9% to 16% depending on the bank

• Most banks require a 15% to 20% down payment

• Tenures range from 1 to 7 years

• Maximum loan amount is typically PKR 3 million

Home Loan Calculator

• Estimates housing loan EMIs for property purchases or construction

• Rates are estimated at 12% to 15% annually

• Tenures can stretch from 5 to 20 years

• Even a small rate difference creates a huge impact over 20 years

Education Loan Calculator

• Helps students plan repayments for university or professional courses

• Breaks down monthly payments into manageable numbers

• Useful for comparing government and private bank education schemes

Business Loan Calculator

• Designed for small business owners and entrepreneurs

• Business loans are often priced at KIBOR + 4% to 4.5%

• Helps project monthly cash flow requirements before borrowing

Here is a quick comparison of typical loan options available in Pakistan:

| Loan Type | Typical Rate (2026) | Max Amount | Max Tenure |

|---|---|---|---|

| Personal Loan | KIBOR + 14-16% | PKR 4 Million | 4 Years |

| Car Loan | 9% - 16% | PKR 3 Million | 7 Years |

| Home Loan | 12% - 15% (est.) | Varies | 20 Years |

| Business Loan | KIBOR + 4-4.5% | Varies | 5-10 Years |

Benefits of Using a Free EMI Calculator

Why should you always use a calculator before taking a loan? Here are the key reasons:

• Saves Time: Manual EMI calculations take 10 to 15 minutes and risk errors. An online calculator gives results in under 3 seconds.

• Ensures Accuracy: The calculator uses the same formula banks use. So your results match what the bank will charge you.

• Helps Compare Lenders: You can compare HBL vs Meezan vs Standard Chartered in minutes, instead of visiting each branch. Bookmark the Mortgage Calculator and Auto Loan Calculator if you are juggling a flat upgrade and a car change in the same quarter.

• Avoids Repayment Surprises: Knowing your EMI in advance means you will never be shocked by your monthly statement.

• Supports Budget Management: You can see if the EMI fits within your monthly income before committing to the loan.

• Reveals True Cost of Borrowing: A calculator shows total interest paid over the loan life. For a PKR 1M personal loan at 16% over 4 years, you pay over PKR 370,000 in interest alone.

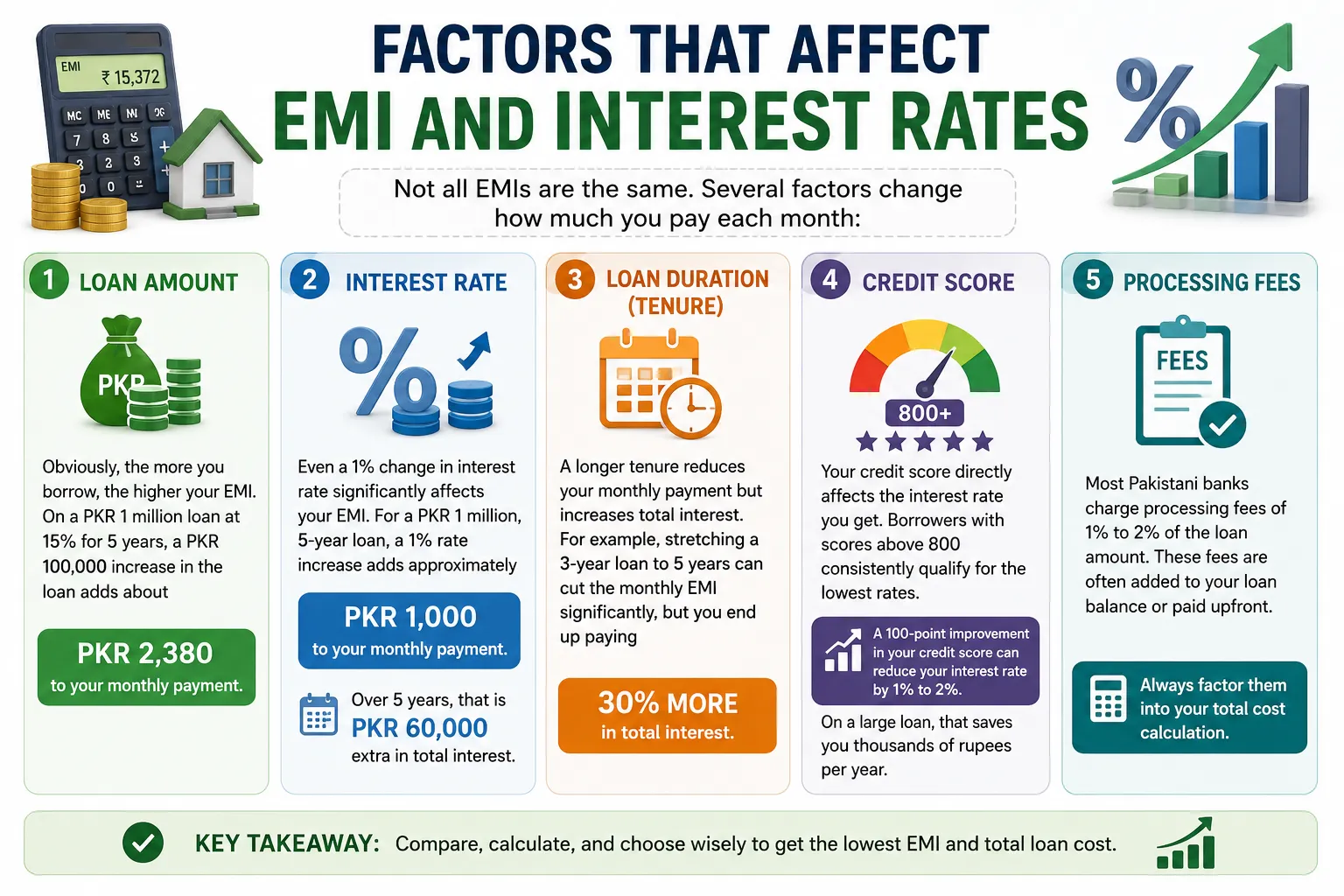

Factors That Affect EMI and Interest Rates

Not all EMIs are the same. Several factors change how much you pay each month:

1. Loan Amount

Obviously, the more you borrow, the higher your EMI. On a PKR 1 million loan at 15% for 5 years, a PKR 100,000 increase in the loan adds about PKR 2,380 to your monthly payment.

2. Interest Rate

Even a 1% change in interest rate significantly affects your EMI. For a PKR 1 million, 5-year loan, a 1% rate increase adds approximately PKR 1,000 to your monthly payment. Over 5 years, that is PKR 60,000 extra in total interest.

3. Loan Duration (Tenure)

A longer tenure reduces your monthly payment but increases total interest. For example, stretching a 3-year loan to 5 years can cut the monthly EMI significantly, but you end up paying 30% more in total interest.

4. Credit Score

Your credit score directly affects the interest rate you get. Borrowers with scores above 800 consistently qualify for the lowest rates. A 100-point improvement in your credit score can reduce your interest rate by 1% to 2%. On a large loan, that saves you thousands of rupees per year.

5. Processing Fees

Most Pakistani banks charge processing fees of 1% to 2% of the loan amount. These fees are often added to your loan balance or paid upfront. Always factor them into your total cost calculation. If you are also wondering how inflation changes what that EMI feels like, pair this check with an Inflation Calculator.

Tips to Reduce Your Loan EMI

Fortunately, you have several practical ways to lower your monthly payment:

| Tip | How It Helps | Example Impact |

|---|---|---|

| Choose a Longer Tenure | Spreads payments over more months | EMI drops but total interest rises by ~30% |

| Make a Higher Down Payment | Reduces the principal you borrow | 20% down on a car loan saves PKR 4,000-5,000/month |

| Improve Your Credit Score | Qualifies you for lower interest rates | 100-point score gain = 1-2% rate reduction |

| Compare Lenders | Different banks offer different rates | Rate gap of 2-3% saves PKR 50,000+ over a 5-yr loan |

| Refinance Your Loan | Replace high-rate loan with lower rate | Can cut EMI by 10-20% if rates have fallen |

The smartest approach is to combine multiple tips. For example, improving your credit score AND making a 20% down payment can dramatically reduce both your EMI and your total interest cost.

Loan Calculator vs. Manual Calculation

Some people still try to calculate EMI by hand. Here is why the online calculator always wins:

| Feature | Loan Calculator | Manual Calculation |

|---|---|---|

| Speed | Instant (under 3 seconds) | 10-15 minutes |

| Accuracy | High — uses exact formula | Risk of errors |

| Ease of Use | Beginner-friendly | Requires math knowledge |

| Scenario Testing | Try multiple options quickly | Starts over each time |

| Cost | 100% Free | Free but time-consuming |

As you can see, there is simply no reason to calculate EMI manually. The online tool is faster, more accurate, and completely free to use. When you move on to surplus cash or retirement pots, the Investment Calculator is a natural next stop.

Frequently Asked Questions (FAQs)

What is EMI in a loan?

EMI stands for Equated Monthly Installment. It is the fixed amount you pay to your bank every month until your loan is fully repaid. Each EMI includes a portion of the principal and a portion of the interest.

How accurate are online loan calculators?

Online loan calculators are highly accurate because they use the same mathematical formula that banks apply. The results you see will closely match your actual bank statement. Small differences may occur due to rounding or bank-specific processing fees.

Can I calculate home and car loans together?

Yes. You can run the Mortgage Calculator and Auto Loan Calculator separately, then add the EMIs together to see your total monthly loan burden. This is especially useful if you are planning to take more than one loan at the same time.

Does EMI change with interest rates?

For fixed-rate loans, your EMI stays the same throughout the loan term even if market rates change. However, for variable-rate loans (linked to KIBOR), your EMI can change when the benchmark rate moves up or down.

Are loan calculators free to use?

Yes. A good loan calculator is 100% free and requires no sign-up or registration. You can use it as many times as you like without any cost.

What is KIBOR and why does it matter?

KIBOR stands for Karachi Interbank Offered Rate. It is the benchmark interest rate used in Pakistan's banking system. Most variable-rate loans are priced as KIBOR plus a fixed percentage. When KIBOR goes up, your variable-rate EMI increases too. As of early 2026, KIBOR is in the 10-12% range, which is why personal loan rates are so high. An Inflation Calculator helps translate that macro story into everyday purchasing power.

Conclusion

A free loan calculator is not just a convenience. It is an essential tool for anyone who wants to borrow smartly.

Before you walk into any bank in Pakistan, take five minutes and run the numbers. Check your EMI. Compare the rates. Look at the total interest cost over the full loan term. The information you gain will give you real negotiating power.

Remember these key takeaways:

• Always calculate EMI before applying for any loan

• Compare at least three banks before making a decision

• A higher down payment and better credit score reduce your costs significantly

• Longer tenures lower monthly EMI but increase total interest paid

• Free online calculators are just as accurate as the tools banks use

Smart financial decisions start with accurate information. Use the calculator, know your numbers, and never borrow more than you can comfortably repay. When you pivot from debt to growth, the Investment Calculator and Inflation Calculator round out the same planning session.